The Silicon Photonics Light Source War: Same Problem, Three Solutions (Small Cap)

Intro

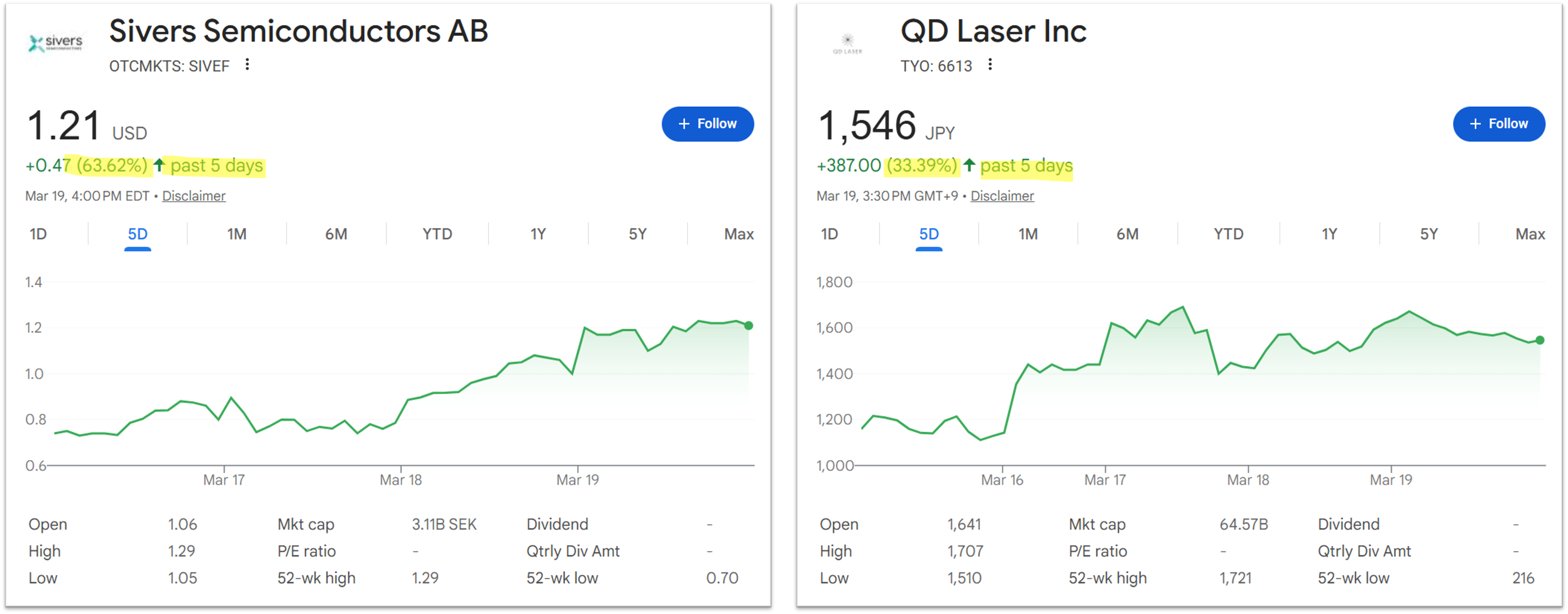

Sivers Semiconductors (OTCMKTS: SIVEF) surged +63.62% and QD Laser (TYO: 6613) jumped +33.39% over the past five days. What do these two microcaps have in common? They’re both light source suppliers for silicon photonics (SiPho).

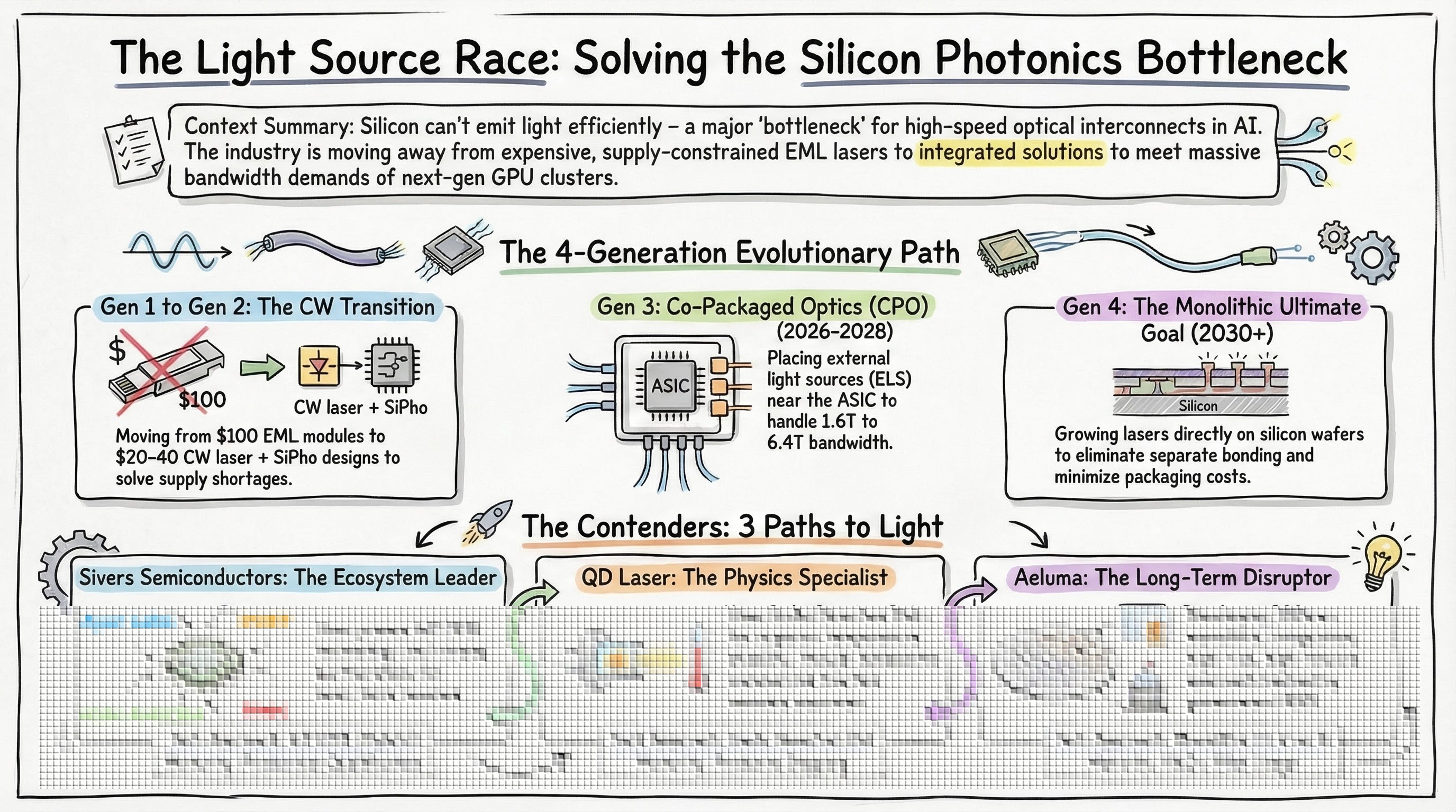

Silicon photonics has a fatal weakness. Silicon can’t efficiently generate light. It’s an indirect bandgap material. You can make waveguides, modulators, and even detectors (by adding germanium), but the one thing you can’t make from silicon or silicon nitride (SiN) alone is a laser.

So every SiPho chip needs a III-V compound semiconductor (InP, GaAs, etc.) laser source attached to it from the outside. This “light source integration” problem is the most fundamental bottleneck in SiPho. It’s the primary reason packaging costs are high, form factors are large, and yields are lower than they should be.

Different approaches mean different risk-reward profiles. Japan-based QD Laser (TYO: 6613) uses GaAs-based quantum dot (QD) lasers, Sweden-based Sivers Semiconductors (STO: SIVE / OTCMKTS: SIVEF) uses InP-based DFB lasers, and US-based Aeluma (NASDAQ: ALMU) is growing III-V materials directly on 300mm silicon wafers through monolithic integration.

Today I’ll examine these two surging stocks alongside Aeluma, comparing all three across technology, strategy, and financials, while mapping the full optical module architecture from Gen 1 (EML) through Gen 4 (monolithic).

1. Background: Why SiPho Light Sources Matter Right Now

As AI datacenters scale, demand for optical interconnects is growing rapidly. Bandwidth requirements between GPU clusters are climbing from 800G to 1.6T, 3.2T, and eventually 6.4T. Copper wiring simply can’t keep up on power efficiency and distance.

The mainstream approach today is pluggable transceivers. But as bandwidth climbs, traditional pluggables based on externally modulated lasers (EMLs, Electro-Absorption Modulated Lasers) are hitting their performance ceiling [28]. Next-gen GPU architectures are pushing toward co-packaged optics (CPO), and CPO requires external light sources (ELS).

For a sense of market scale: LightCounting estimates the total integrated optical device market will reach approximately $30B by 2026, with SiPho-based products accounting for roughly half of that [2]. Northland Capital Markets analyst Tim Savageaux sees the ELS market alone as a $1B+ annual opportunity [3].

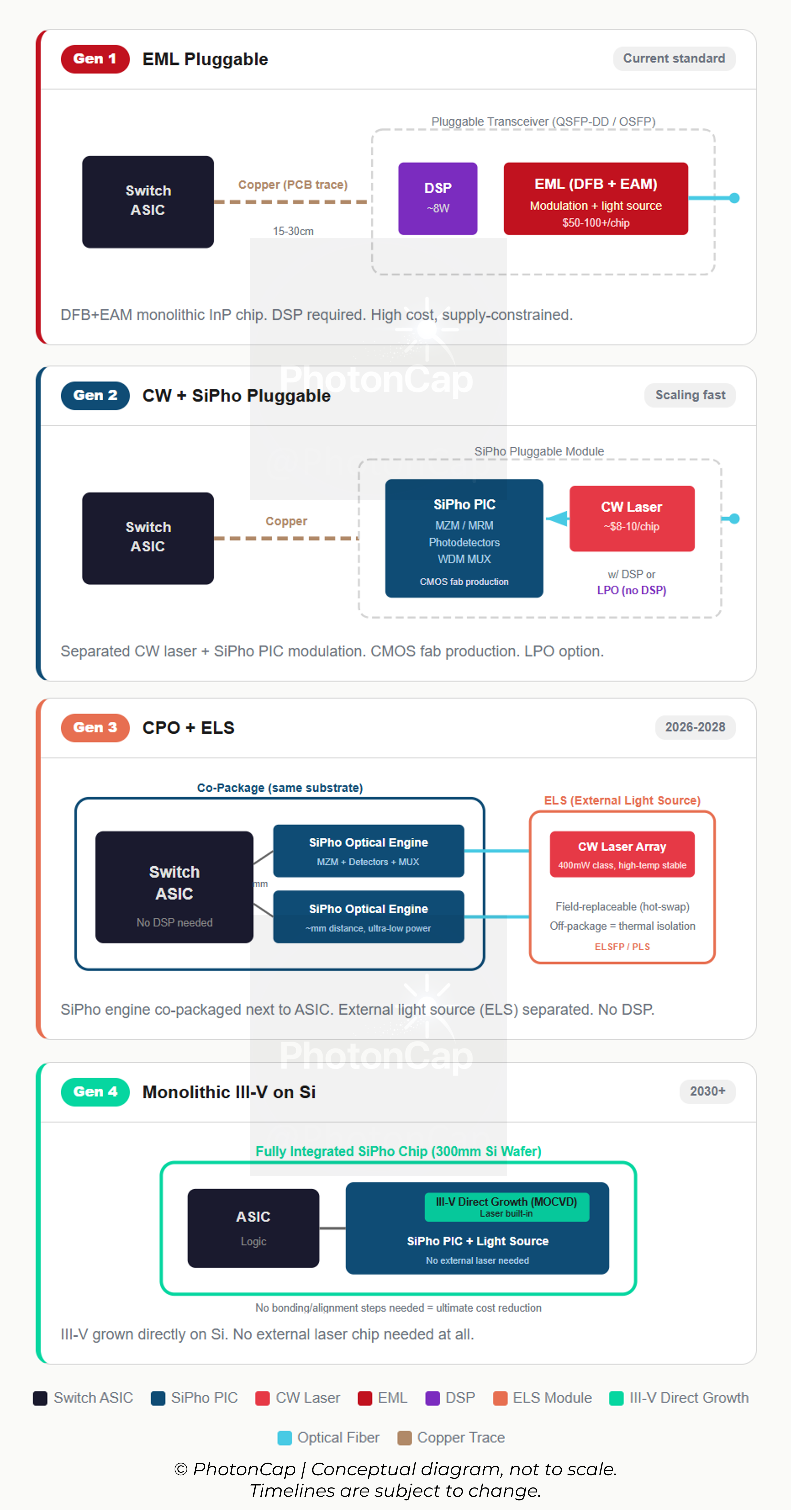

This brings us to the key question. How do you build the light source, and how do you deliver it to the SiPho chip? Datacenter transceiver light source architectures sit on a multi-generational evolutionary path. Understanding this framework is essential to seeing where the three companies fit.

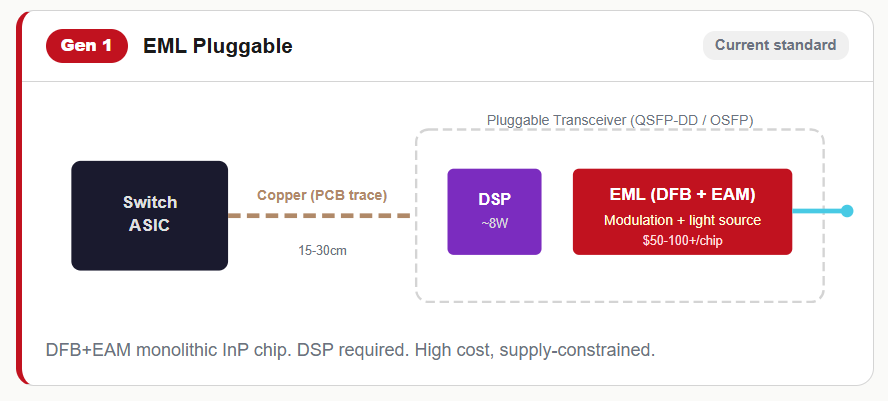

Gen 1: EML (current standard, InP pluggable, supply-constrained)

An EML (Electro-Absorption Modulated Laser) integrates a DFB laser and an electro-absorption modulator (EAM) onto a single InP chip. The laser generates light and modulates data simultaneously. Modulation quality is high (low chirp), making it ideal for longer-reach transmission. It’s the current standard for 800G DR8 and 1.6T modules.

The problem is power consumption, heat, and cost/supply. An 800G EML module requires eight 100G EML lasers at ~$10+ each, bringing the laser cost alone to $80-100+ per module [28][29]. On top of that, NVIDIA has pre-allocated massive capacity from key suppliers like Lumentum and Coherent, pushing delivery lead times beyond 2027 for non-NVIDIA customers [28]. Estimates suggest 800G transceiver production could fall 40-60% short of demand through 2027 [28]. The Buy American momentum combined with this capacity crunch likely explains the recent sharp rally in Applied Optoelectronics (NASDAQ: AAOI), one of the few US-based EML producers with domestic manufacturing.

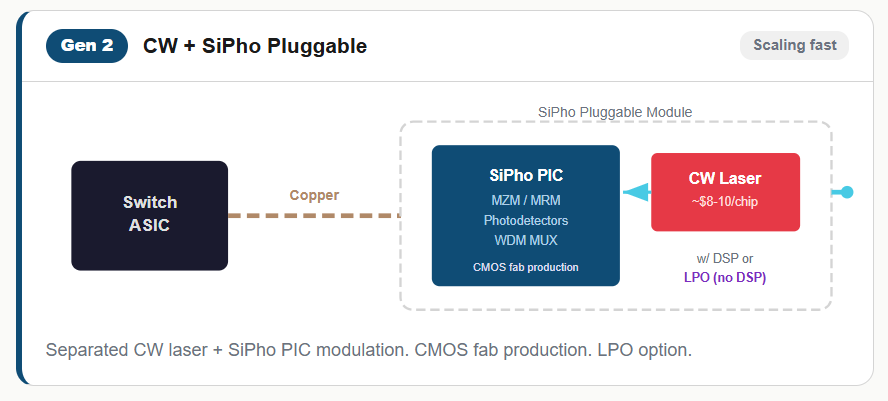

Gen 2: CW laser + SiPho (the EML alternative, scaling fast)

A CW (Continuous Wave) laser is a simple DFB laser that emits a steady, unmodulated beam. Think of it as a lightbulb that just shines constant light. The CW laser sits externally, while modulation, reception, wavelength multiplexing, and other optical functions are handled by the SiPho PIC. Data modulation is performed by either MZM (Mach-Zehnder Modulator) or MRM (Micro-Ring Modulator) on the SiPho chip. MZM splits light into two arms and uses phase differences to create constructive/destructive interference, encoding 1s and 0s. MRM uses a resonant structure for a smaller footprint and lower power, but is more temperature-sensitive and requires active feedback control [30].

The key advantage is cost reduction and high-volume production through CMOS processes. CW lasers are far simpler than EMLs, costing only ~$8-10 per chip, and multiple suppliers can produce them. A typical 800G/1.6T SiPho module requires 2-4 CW light sources (~70mW for 800G, ~100mW for 1.6T), bringing the total laser cost per module to just $20-40, less than half of the $80-100+ for EML-based modules [29]. The SiPho chip can be manufactured at CMOS fabs like GlobalFoundries, Tower, and TSMC, providing excellent scaling [30].

However, since this is still a pluggable form factor, electrical signals must travel from the switch ASIC to the front-panel transceiver over copper PCB traces. The signal loss over this distance and the power consumption of DSP/retimers to compensate for it are substantial. Of course, InP substrates for the CW lasers themselves still depend on a small number of suppliers like Sumitomo and AXT (NASDAQ: AXTI).

This DSP power problem gave rise to LPO (Linear Pluggable Optics). LPO removes the DSP entirely from inside the pluggable module, relying instead on the switch ASIC’s SerDes signal conditioning. The module’s TIA (Transimpedance Amplifier) and Driver operate in linear mode, simply passing the signal through. Since CPO adoption faces high barriers in packaging complexity, chiplet ecosystem maturity, and test/yield, LPO emerged as a pragmatic bridge: “skip the DSP, stretch pluggables through the 800G-1.6T generation.” The tradeoff is interoperability: without DSP signal conditioning, performance can vary across different host platforms.

The EML shortage is accelerating the CW+SiPho transition. LightCounting projects SiPho-based transceivers will exceed 50% market share by 2026 (up from 33% in 2024) [30]. Both Sivers’ InP DFB lasers and QD Laser’s quantum dot lasers are positioned as CW light source suppliers in this architecture. That said, I have some reservations about whether QD Laser’s quantum dot lasers have actually secured a competitive position in the SiPho datacenter market. More on this later.

Gen 2.5: NPO (Near-Packaged Optics, transitional)

A transitional step before full CPO. The optical engine moves from the switch front panel onto the main board near the ASIC, shortening electrical trace length. What’s notable is that Broadcom’s NPO uses VCSELs (Vertical-Cavity Surface-Emitting Lasers), not SiPho+CW lasers [36]. It operates over multimode fiber (MMF) for short-reach AI scale-up links (a few meters). Compared to CPO’s SiPho engines, VCSEL-based NPO is far simpler to package and leverages existing VCSEL supply chains and MMF infrastructure for faster production ramp. At OFC 2026, Broadcom announced a 3.2T VCSEL-based NPO solution [36].

The tradeoff: VCSELs are limited in reach and bandwidth due to their multimode nature, so rack-to-rack and longer distances still require SiPho-based CPO (Gen 3). NPO is a pragmatic bridge: “get past the copper wall without CPO’s complexity.”

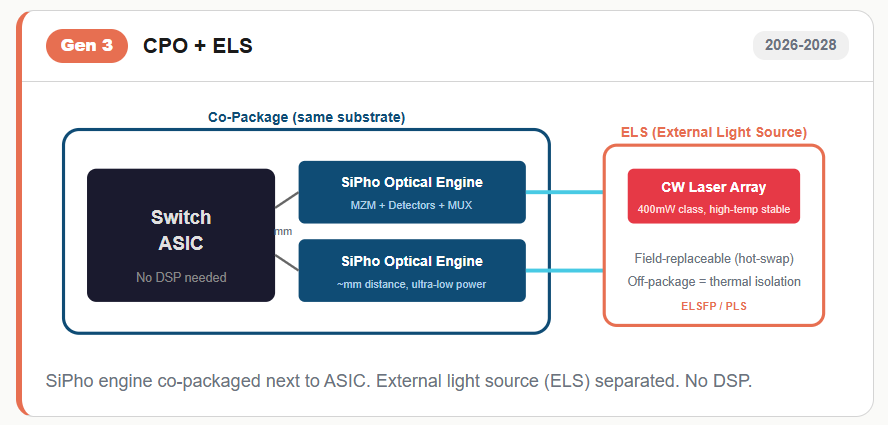

Gen 3: CPO + ELS (next-gen, 2026-2028 ramp)

In co-packaged optics (CPO), the SiPho engine sits right next to the switch/GPU ASIC on the same substrate. But lasers are temperature-sensitive, so instead of placing them next to the hot ASIC, you put them in a separate module outside the package. That’s the external light source (ELS) [31].

Separating the laser means you can replace it if it fails, and thermal management improves. Several major products use this architecture: NVIDIA’s Quantum-X800 CPO (InfiniBand, TSMC COUPE SiPho platform + Lumentum lasers, shipping H2 2025), Broadcom’s Bailly (TH5-based 51.2T CPO Ethernet switch, the industry’s first volume-production CPO), and Marvell’s TX9190 (Teralynx-based liquid-cooled CPO switch, demoed with Jabil at OCP 2025) [30][31]. Broadcom is already shipping its next-gen CPO, TH6-Davisson (102.4Tbps, 200G/channel, TSMC COUPE) [35]. CPO ELS demands much higher output power (400mW class, roughly 4x standard CW) and stable operation at high temperatures (50C+) [30]. For more on why NVIDIA invested $4B in Coherent/Lumentum and a comparison of laser/optical module company specs, see my previous article [33].

NVIDIA's $4 Billion Photonics Bet: Broadcom Wasn't Wrong — But the Market Completely Misread the Signal

1. Introduction: The Announcement and the Market’s Reaction

The POET-Sivers partnership targets exactly this Gen 3 architecture [1]. QD Laser’s quantum dot lasers have excellent high-temperature stability in theory, but their current product output (5-16mW) is far below ELS requirements (400mW class), making near-term ELS market entry unlikely.

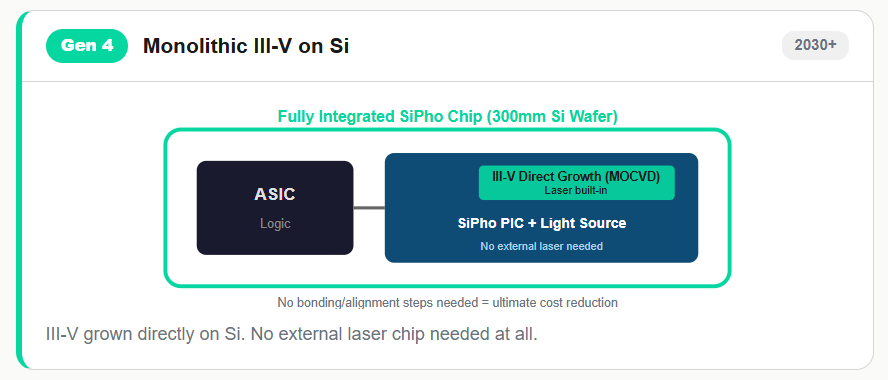

Gen 4: Monolithic III-V on Si (long-term, 2030+)

Growing III-V material directly on the Si wafer so no separate laser chip is needed at all. Instead of the “external laser + SiPho chip” approach of Gen 2/3, the laser is built into the SiPho chip itself. If successful, it minimizes packaging cost and achieves ultimate scalability, but lattice mismatch and defect density challenges are still being resolved.

Aeluma is betting directly on Gen 4.

Where the three companies sit

Architecture Timeline QD Laser Sivers Aeluma Gen 2. CW + SiPho pluggable Mainstreaming now CW source (QD CW) Core position (InP DFB CW) N/A Gen 3. CPO + ELS 2026-2028 Power gap limits near-term entry POET partnership N/A Gen 4. Monolithic 2030+ Related foundational tech N/A Core position

Key takeaway: Light source architecture is evolving from Gen 1 (EML) to Gen 2 (CW+SiPho) to Gen 3 (CPO/ELS) to Gen 4 (monolithic). The EML shortage is accelerating this transition, and the three companies are positioned at different stages along this evolutionary path.